A Recession Not Certain

The U.S. economy entered 2025 with notable momentum. First-quarter indicators showed strong consumer spending, firm labor markets, and stable corporate investment. However, this constructive start has been overshadowed by a sharp escalation in trade tensions. The imposition of broad new tariffs — including a universal 10% import tariff and increased levies on specific trading partners — now threatens to disrupt supply chains, suppress demand, and derail both U.S. and global growth.

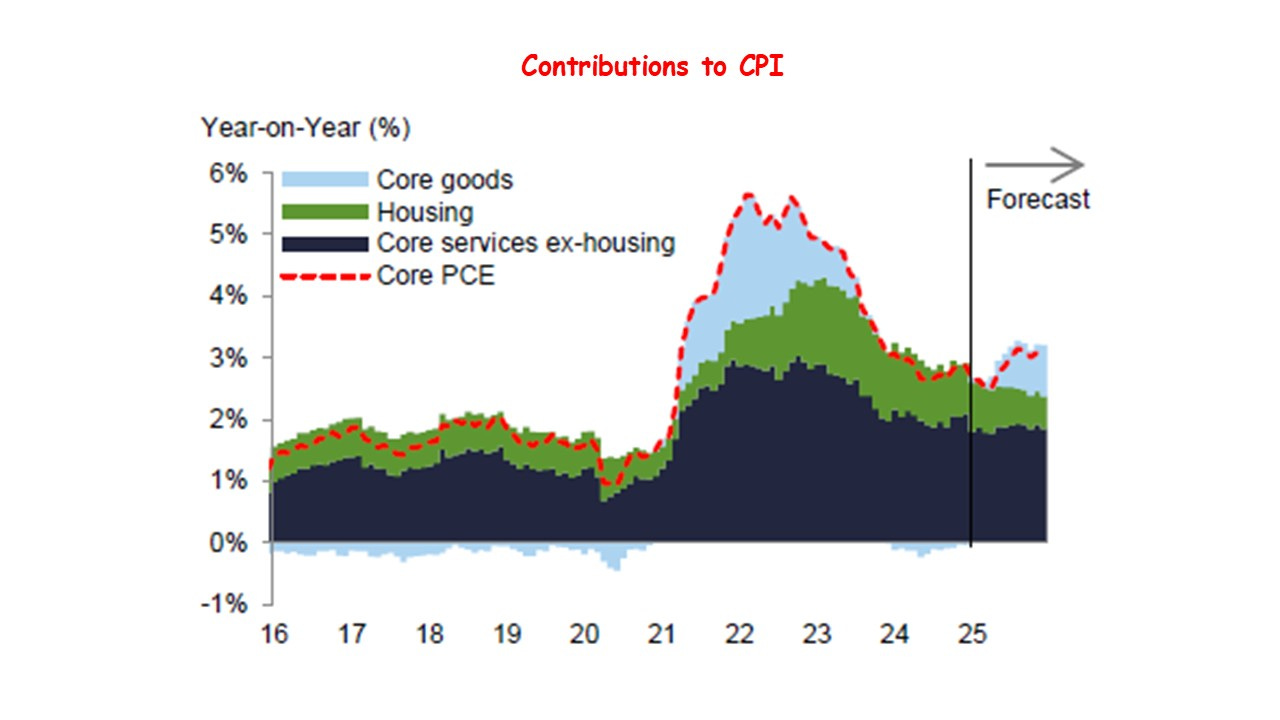

Tariffs, as they are currently designed, have the potential to reverse recent deflationary trends in goods prices. Until now, inflationary pressures had been concentrated largely in the services sector — especially in areas such as healthcare, education, and hospitality — driven by structural labor shortages and rising wages. In contrast, goods prices remained relatively tame as supply chains recovered from the pandemic-era dislocations. That trend is now changing. Higher import duties are expected to raise input costs for manufacturers and consumer prices across a wide range of products, reigniting inflation and eroding real household incomes.

This shift presents a growing dilemma for monetary policy. The Federal Reserve now finds itself caught between countervailing risks. On the one hand, inflation expectations may firm due to rising goods prices, pressuring the Fed to hold interest rates steady or even tighten further. On the other hand, the signs of slowing demand, falling asset prices, and weakening business confidence suggest the need for monetary easing. The Fed’s challenge is that of a goalkeeper in a penalty shootout — lean left to prevent inflation from getting out of control, or dive right to cushion the economy from recession. Either direction carries risks, and the margin for error is narrow.

The broader context for this policy tightrope is also evolving. Recent equity market corrections have undermined household wealth. This "wealth effect" could weigh heavily on consumer spending over the coming quarters. Simultaneously, many businesses, concerned about potential demand and rising costs, are likely to postpone or reduce capital expenditure, further weakening the investment outlook.

However, the picture is not uniformly bleak. Several positive offsets are in play, which may mitigate the downside risks.

First, fiscal policy is moving into a more expansionary phase. The administration has proposed renewing and broadening the 2017 tax cuts, with added provisions aimed at boosting middle-income purchasing power. These include tax relief for service-related income such as tips, reductions in Social Security payroll taxes, and more generous depreciation allowances for capital equipment. Such measures could offer timely stimulus, encouraging both household consumption and business investment.

Second, the White House has committed to a wide-ranging deregulation effort aimed at lowering compliance burdens and improving the business environment. Targeted primarily at sectors like energy, finance, and manufacturing, deregulation could unleash productivity gains, ease hiring constraints, and enhance competitiveness.

Third, the administration has shown subtle signs of flexibility related to the tariffs. There are tariff negotiations with a number of trading partners. Industry groups have reported quiet consultations about exemptions, phased rollouts, and selective relaxations of tariff rules. If followed through, such adjustments could limit the economic fallout and help restore investor confidence.

Another source of resilience comes from the composition of the U.S. economy itself. Roughly 80% of U.S. GDP is derived from services — industries that are largely insulated from international trade disruptions. Unlike manufacturing and goods production, service sectors tend to be more domestically anchored and less vulnerable to external shocks. This structural composition provides a stabilizing buffer, reducing the likelihood of a deep or prolonged recession.

In addition, the depreciation of the U.S. dollar in early 2025 introduces a mixed, but potentially supportive, macroeconomic force. A weaker dollar — now at its lowest level in three years — helps make American exports more competitive and dampens the appetite for foreign goods, potentially narrowing the trade deficit. This could offer a partial offset to growth headwinds. At the same time, a sustained dollar decline may add to inflationary pressure by increasing the cost of imports, especially for raw materials and key imports. It also raises the specter of diminished global demand for U.S. assets, which could complicate funding for fiscal deficits and place upward pressure on long-term interest rates.

Taken together, these factors paint a picture of an economy at a pivotal juncture. The positive momentum of early 2025 remains alive but increasingly fragile. Tariff shocks and inflation dynamics are intersecting with global capital flows and domestic policy choices in ways that could tip the balance toward stagnation or continued expansion. Much will depend on how deftly policymakers respond to the challenges at hand.