Can Stagflation Return?

Can Stagflation Return?

Recent economic data indicate that economic growth is moderating, and the labor market is cooling. However, the inflation rate is struggling with the "last mile" problem. Some worry this might be the beginning of stagflation, which would be bad news for the stock and bond markets. What does history say about stagflation, and how likely is it this time around?

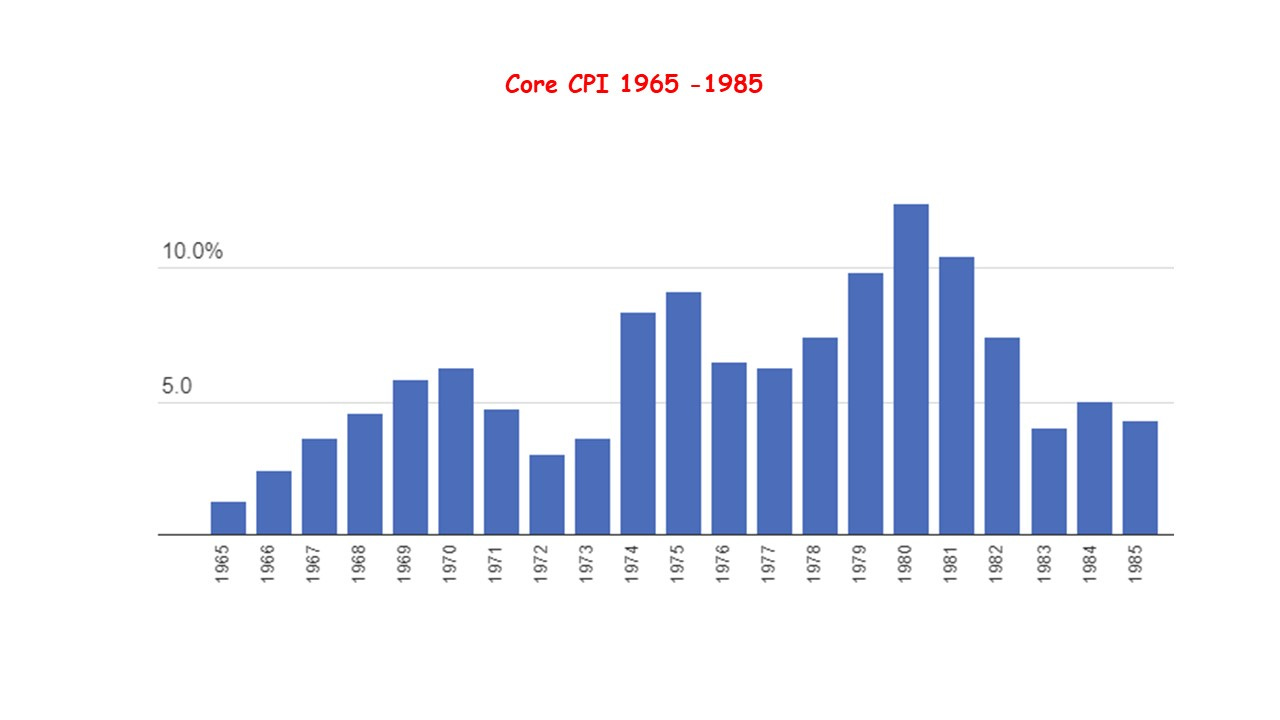

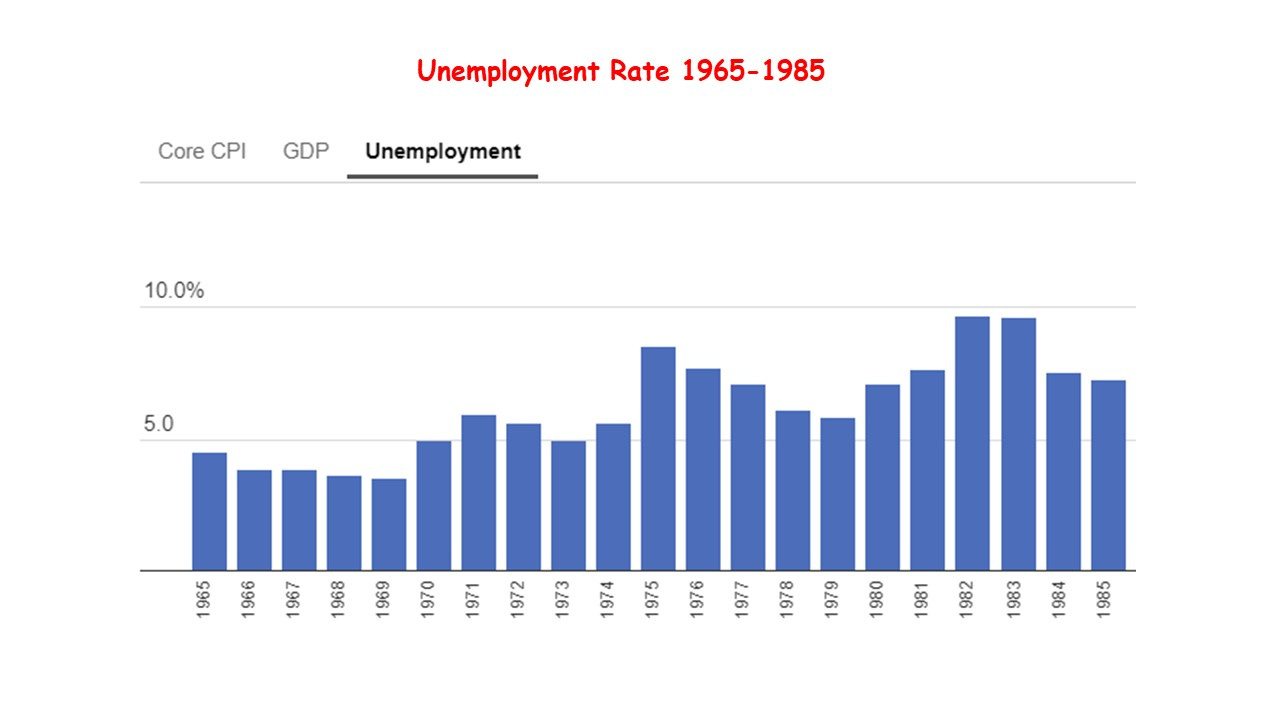

Stagflation in the 1970s and 1980s was characterized by the simultaneous occurrence of high inflation, high unemployment, and stagnant economic growth. This phenomenon was troubling because it contradicted traditional economic theories, such as the Phillips Curve, which suggested that inflation and unemployment were inversely related. Several factors contributed to stagflation.

The first major factor was the oil embargo imposed by the Organization of Petroleum Exporting Countries (OPEC) in 1973. OPEC reduced oil production and placed an embargo on oil exports to the United States and other countries that supported Israel during the Yom Kippur War. This led to a sharp increase in oil prices, quadrupling from around $3 to $12 per barrel. A second oil shock occurred in 1979 due to the Iranian Revolution, which disrupted oil supplies and caused another spike in oil prices.

The increase in oil prices significantly raised production costs for businesses, leading to higher prices for goods and services (inflation). At the same time, these higher costs caused many businesses to reduce output and lay off workers, contributing to higher unemployment.

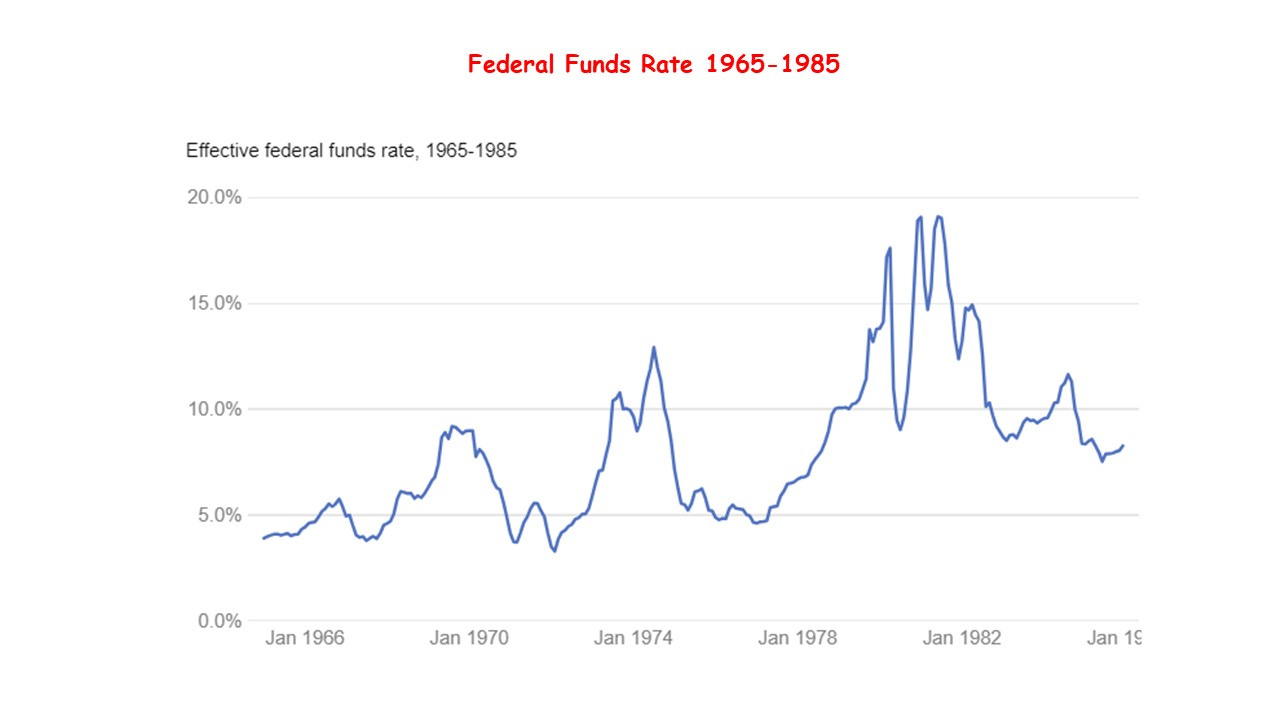

In response to inflationary pressures, central banks, particularly the Federal Reserve in the United States, implemented tight monetary policies, raising interest rates to curb inflation. However, this also slowed economic growth and increased unemployment, exacerbating the stagflation problem.

As inflation rose, workers demanded higher wages to keep up with the rising cost of living. Businesses, in turn, raised prices to cover the higher wage costs, leading to a wage-price spiral that further fueled inflation.

The experience of stagflation led to a reevaluation of economic theories and policies. Monetarist theories, championed by economists like Milton Friedman, gained prominence, emphasizing the role of monetary policy and the control of the money supply to manage inflation. In the United States, the Federal Reserve, under Chairman Paul Volcker, adopted a strict anti-inflationary stance in the late 1970s and early 1980s, raising interest rates to very high levels. This policy eventually succeeded in bringing down inflation but at the cost of severe recessions and high unemployment in the early 1980s.

How likely is stagflation this time around? To begin with, the U.S. is a net oil exporter and is less vulnerable to oil shocks from geopolitical conflicts. There is no wage-price spiral, even though labor costs have been rising significantly, contributing to service inflation. Productivity gains have been higher than expected, and as AI and technology are more widely adopted, productivity should further benefit. Not surprisingly, profit margins at businesses are very healthy, leading to more investment and hiring. The most important factor is the credibility of the central bank as an inflation fighter. Before the pandemic, the central bank’s credibility was high as the Federal Reserve kept inflation contained. Around the pandemic, this credibility was damaged as astronomical government spending was financed by printing money. Recently, however, the central banks' credentials as inflation fighters have received a boost.

While there are concerns about persisting inflation and potential slowdowns in economic growth, the current economic environment differs significantly from the 1970s and 1980s. While stagflation is a possibility, it is not inevitable, and hopefully proactive policy measures can help mitigate the risk.