The Inflation Picture Continues to Improve

The Inflation Picture Continues to Improve

Without shelter only 1.35 percent

The Inflation Picture Continues to Improve

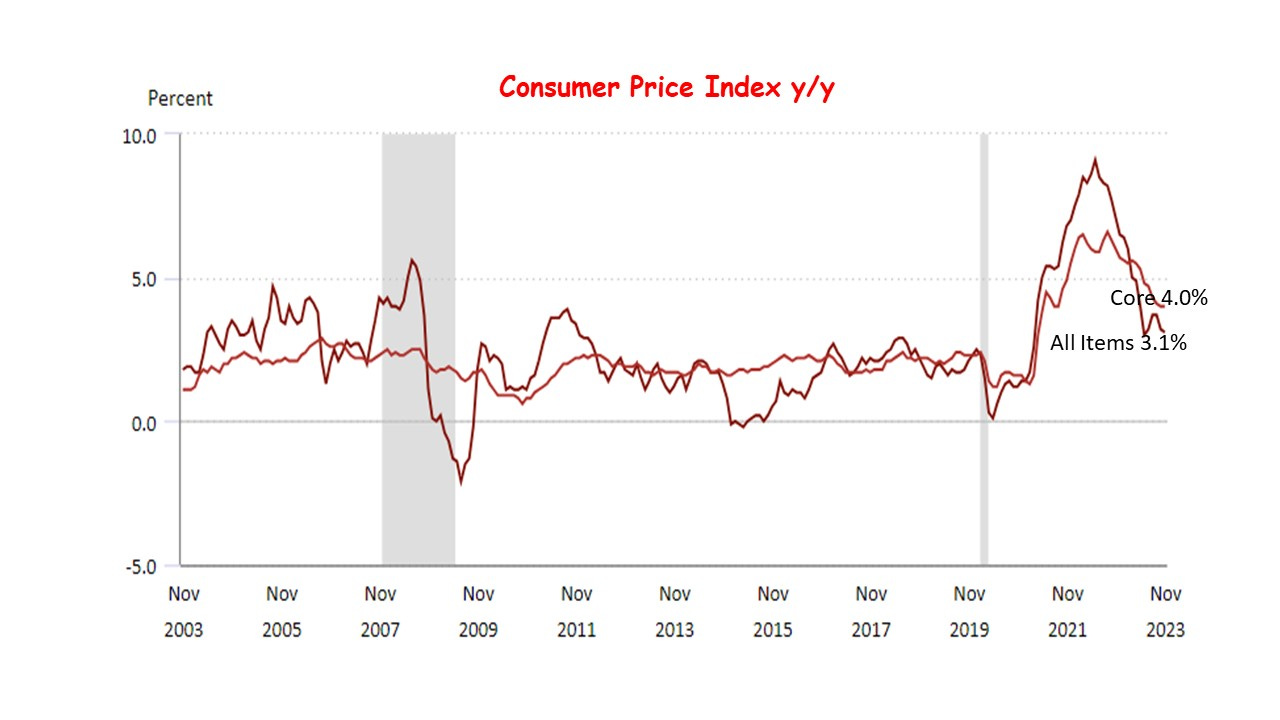

The inflation picture remained stable for November rising 3.1 percent from a year ago, slightly down from 3.2 percent in October. The core rate, which excludes volatile food and energy, remained unchanged at 4.0 percent from a yar ago. The Federal Reserve’s FOMC is meeting today and tomorrow. Although it is not quite “Mission Accomplished” yet, the overall trend is downward at a faster pace than anticipated. Even though chairman Powell won’t say it in public, the cooling inflation trend has made interest rate cuts sometime during the first half of 2024 likely.

Goods prices, such as used cars, appliances, and furniture, have been falling, while service costs including food away from home with heavy labor component, leisure and medical care have been increasing. Shelter, one of the main drivers of inflation, has risen 6.5 percent from a year ago, explaining about half of the price increase for the month.

In terms of inflation dynamics, the economy is currently experiencing both disinflation (a slowdown in the rate of price increase) and deflation (an actual decrease in price). The pandemic era saw a surge in consumer spending, leading to shortages of goods from vehicles to clothing. In February 2022, the inflation rate for durable goods rose at 10.7 percent, a 47-year peak. A study by the San Francisco Federal Reserve Bank attributes approximately half of the pandemic's inflation to the supply shortages.

Fortunately, the economy has moved past these shortages. The prices of various commodities, including lumber, copper, energy, appliance, furniture and used cars have been falling, indicating temporary deflation. Walmart projects that the price for about half of its non-food merchandise could decrease in the upcoming months. This trend, if continued, could exert downward pressure on the overall inflation rate.

The other significant contributor to inflation is the demand side. The price of services ranging from healthcare to personal care, which rely heavily on labor, has been rising due to the tight labor market. Increased employment and wages as well as the delayed effects from the massive government spending and the monetization of the Federal debt have boosted demand for travel, leisure, and dining out. However, the recent hikes in interest rates have subdued this demand, slowing down the rate of price increases for these services.

Shelter costs, which have 34 percent weight in the Consumer Price Index (CPI), are another area where deflation might occur. Between November 2022 and November 2023, the overall CPI rose by 3.1 percent. However, excluding the shelter component, the CPI increase was only 1.35 percent, highlighting shelter's significant impact on the overall inflation.

While the rent component of the CPI continues to rise, sources like Zillow and Apartment Rents indicate that actual rents have been falling for some time. Due to the government's method of calculating the shelter index, there's a 6 to 12-month lag in reflecting actual rent changes in the CPI. Since actual rents have been falling, it's expected that soon this trend will be mirrored in the CPI, potentially reducing the inflation rate.

In conclusion, the Federal Reserve is not yet ready to declare a victory. At the end of the FOMC meeting tomorrow, the policymakers will stand pat. The core inflation rate remains significantly above the central bank's 2 percent target. However, the current inflation trend indicates significant progress towards this goal, raising expectations for lower interest rates in 2024.