The Real Story Behind Rising Credit Card Debt

The Real Story Behind Rising Credit Card Debt

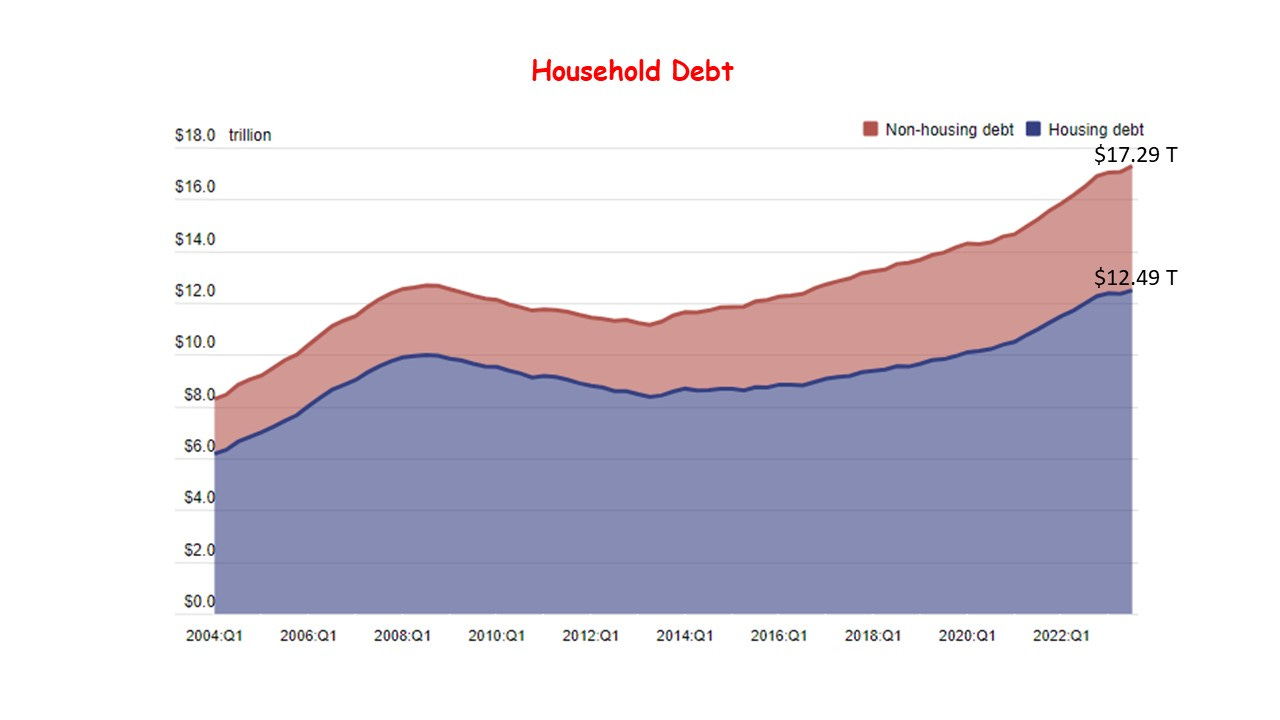

Consumers have increasingly turned to credit cards to make ends meet, leading to a notable rise in debt levels. Despite assumptions that delinquency rates have humped, the reality is somewhat different. Breaking down the figures, American consumer debt reached a staggering $16.84 trillion in the second quarter of 2023, climbing 4.5% from the previous year. This hike is largely driven by substantial increases in credit card debt, which soared by 16.3%, and personal loan debt, which rose by 21.3%. Auto loans also grew by 5.8% due to inflated car prices. Mortgages account for two-thirds of this consumer debt, while non-mortgage debt, including credit cards and home equity lines, make up just 4.8%. Looking at delinquencyrates, there's minimal movement in the housing market. Most homeowners areholding onto low-rate mortgages, unaffected by recent interest rate hikes.

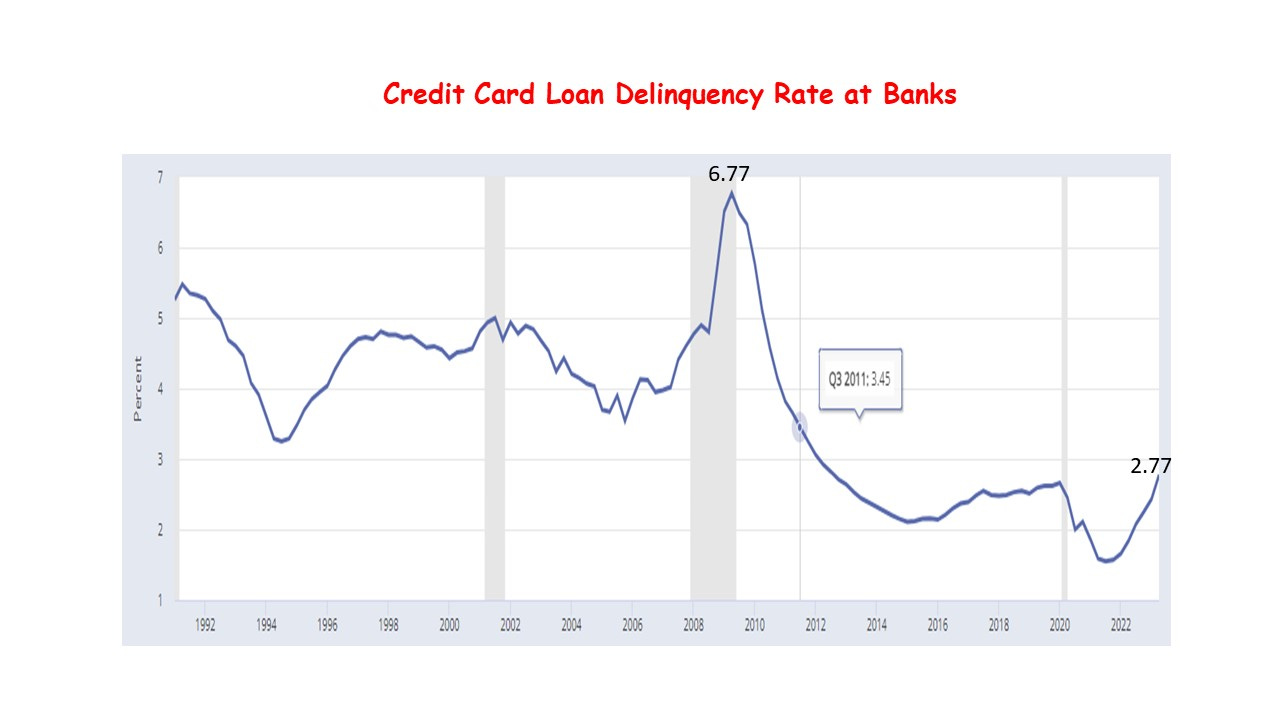

However, for non-housing loans such as credit cards, we see both the volume and interest rates climbing. Yet, the delinquency rates have only modestly increased, due to strong employment and rising wages. Moreover, during thepandemic, the government distributed trillions of dollars to consumers, leadingto what economists’ term "excess savings," which currently stands at around $500 billion.

The surge in credit card debt has multiple origins. During the pandemic's peak, "revenge spending" became a trend, with consumers splurging to make up for lockdown periods, often using credit cards. This was further aggravated by inflation,which pushed up the prices of goods and services, increasing reliance on credit cards. Now, with savings running low, consumers, especially at lower-income households are resorting to credit cards and grappling with high-interest rates—averaging around 19%—that compound their debts and extend repayment periods. These debts disproportionately affect those with lower credit scores, typically linked to lower incomes.

The cost of living has risen faster than wage growth, eroding the purchasing power of many, especially those below the median income. Credit card companies have responded by tightening lending standards, and many cardholders have seen their credit limits shrink since the pandemic began. Generational impacts are also significant; Gen X and millennials face mounting pressures from high prices, elevated spending, and student loan debts. Millennials are hit by rising credit card debts, with younger consumers' balances increasing faster than the overall average. Generation Z, despite their digital savviness, are also under financial stress, often resorting to 'buy now, pay later' habits, contributing to their credit burdens.

Healthcare costs also play a critical role in the rise of credit card debt. High medical expenses lead to delayed care or even “skipped care”, which can worsen health issues. For many, over 10% of household budgets are consumed by healthcare, prompting cuts in essential spending and health care.

In summary, while unemployment remains relatively low, the sharp increase in credit card and personal loan debts, the disproportionate impact on individuals with lower credit scores and lower income, and the struggle to cover rising healthcare costs and living expenses present a growing financial challenge that spans generations.