Time to Dive into Stocks?

Investor optimism in stocks and bonds is currently riding high, buoyed by a series of positive economic indicators and favorable market conditions. Wall Street has embraced a "goldilocks scenario," where inflation appears to have peaked, sliding down from a high of 9 percent in June 2022 to a more manageable 3.2 percent in October. This deceleration has assuage fears of persistent price rises, and some market participants are even pivoting their concerns toward deflation. This is evidenced by the reduction in key prices: energy prices have fallen by 4.5 percent over the past year, used cars by 7.1 percent, and medical care by 2 percent. Retail giant Walmart expects price decreases on numerous retail items.

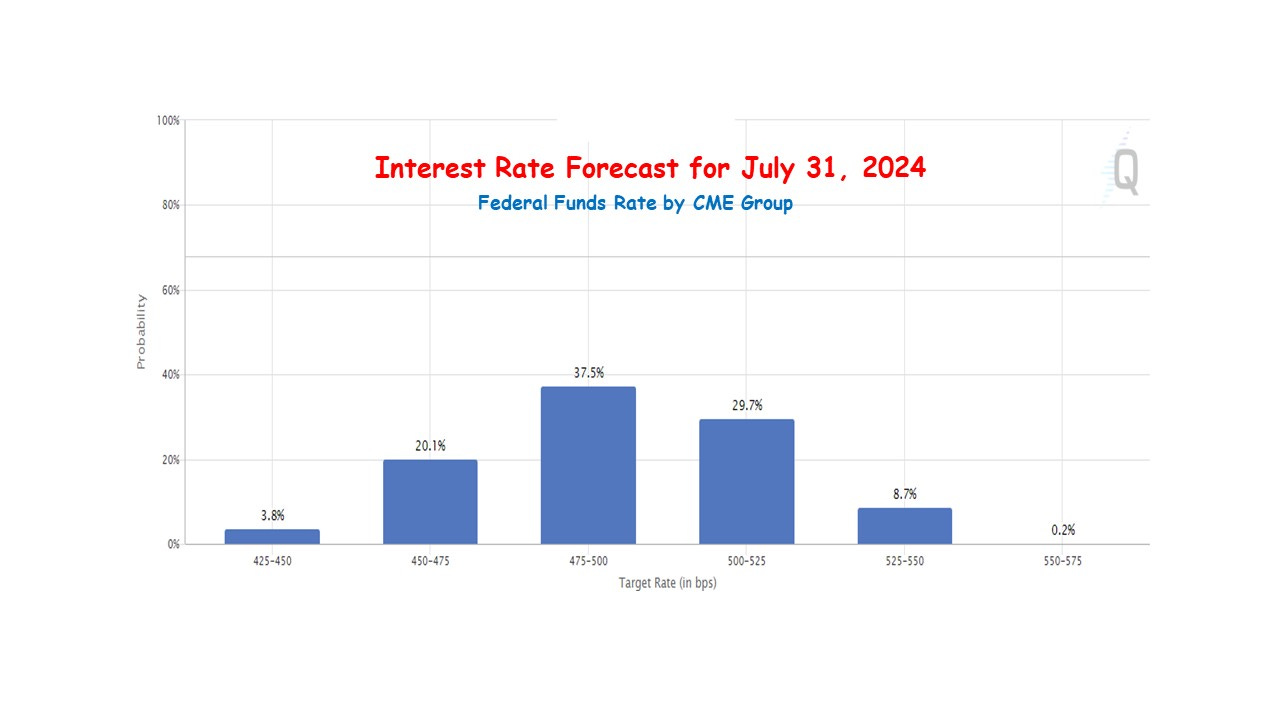

A cooling job market complements the slowing inflation trend, with monthly non-farm employment numbers moderating to 150,000 in October from 324,000 in January. It could be a sign of an economy settling into a sustainable pace, which could influence the Federal Reserve's policy decisions. According to the CME Fed Watch, the central bank will lower the interest rate starting this spring from the current range of 5.25 to 5.50 percent. By the end of July, there is a 61.4 percent probability that the interest rate would be 0.5 percent to 1.0 full percentage point lower. Anticipating this easing of short-term rates, investors are already adjusting their strategies, extending the maturities in their bond portfolios, which has led to a decrease in the 10-year Treasury yield to 4.4 percent from approximately 5 percent just a few weeks prior.

As inflation recedes and sales volumes increase, profit margins are anticipated to stay robust, painting a rosy picture for equities. Less competition from lower bond yields has already benefited stocks. Earnings momentum adds further to optimism, with S&P 500 earnings rising 4.3 percent over the previous year and analysts continually revising earnings expectations upward for the coming year. The consensus among analysts is that S&P 500 earnings could see an increase of 12.2% year-over-year in 2024, with revenues anticipated to rise by 5.6%.

Sector-wise, all eleven sectors of the S&P 500 are expected to report year-over-year earnings growth for 2024. The Health Care sector is predicted to lead with a growth rate of 23.5%, followed by Energy at 21.3%, Communication Services at 16.6%, and Information Technology at a double digit rate.

However, this sunny outlook is not without its potential clouds. The primary concern is that the positive indicators could be a mirage, and the lagged effects of previous tighter monetary policies may yet steer the economy into a recession, rather than the much-hoped-for soft landing. The optimism could be premature, as caution may still be warranted. The recent easing of economic pressures could reverse, or unforeseen events could introduce new challenges. With the global economy interconnected, external shocks could ripple through, undermining current optimism.

Thus, while the current market sentiment is positive, reflecting a belief in continued economic stability and growth, investors would do well to remain vigilant. The balance between optimism and caution is delicate, and the financial markets are known for their unpredictability. The optimism is grounded in concrete data, but history has shown that conditions can change rapidly, and what seems like a sure footing today could become treacherous terrain tomorrow.