Why the Federal Reserve Worries About Rising Real Interest Rate

Why the Federal Reserve Worries About Rising Real Interest Rate

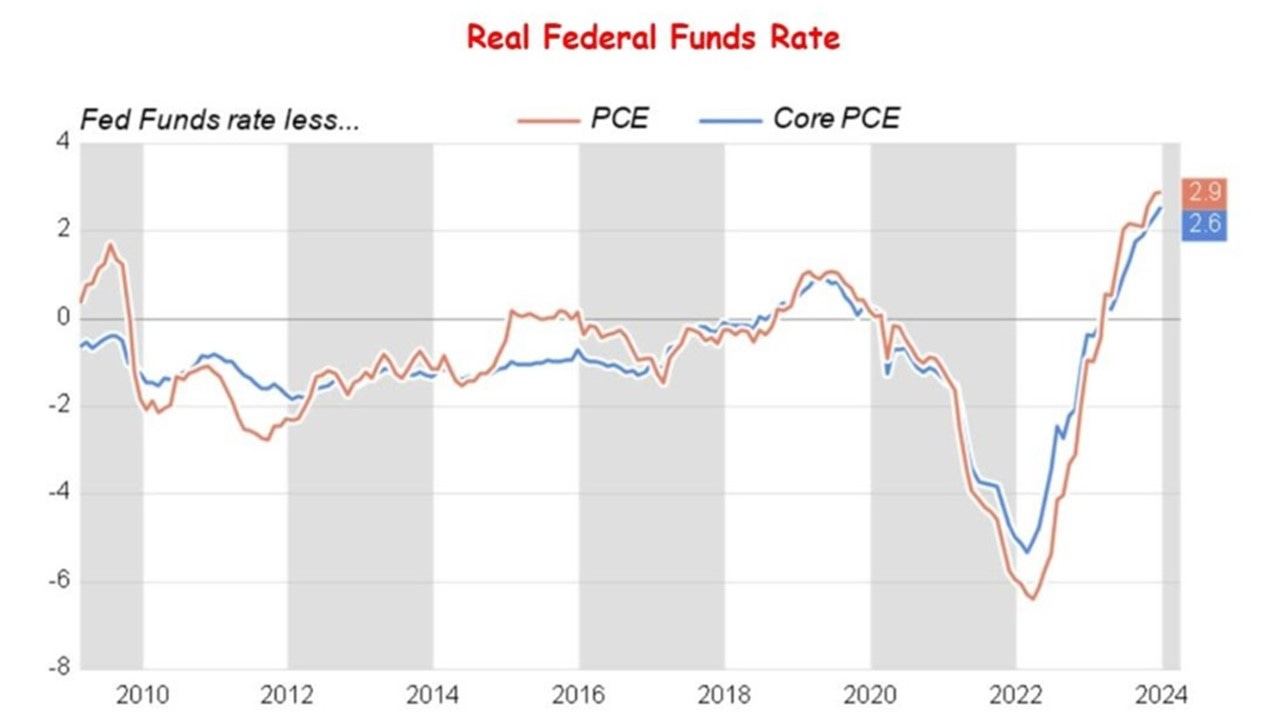

The latest inflation measure favored by the Federal Reserve—the core personal consumption expenditures (PCE)-- has increased 0.4 percent in January up from 0.1 percent in December validating the patient approach to cutting the interest rate by the authorities. One piece of good news is that the inflation gauge compared to a year ago continues to trend down.

Nevertheless, the central bank is still on track to cut the interest rate later this year. The answer lies in the increasing real interest rates—the difference between nominal rates and inflation—which risk slowing economic growth too much. It is well-understood by economists that the decisions of consumers and businesses regarding spending and borrowing hinge on real, rather than nominal, interest rates.

The Federal Reserve manages real interest rates through monetary policy decisions like setting nominal interest rates. By altering nominal rates, they aim to influence real interest rates and, consequently, economic activity, making borrowing more or less attractive based on their economic objectives. However, their control over real interest rates is limited by inflation expectations and international economic factors.

Nominal interest rates are the advertised rates on loans or financial investments, not adjusted for inflation. These rates indicate how much can be borrowed or what the return on an investment will be, disregarding the future purchasing power of the money. In contrast, real interest rates, which are adjusted for inflation, provide a true cost of borrowing or a real yield on investments, accurately reflecting the future purchasing power of the money.

The behavior of consumers and businesses is influenced by real interest rates since these rates determine the actual (inflation-adjusted) costs and benefits. Low real interest rates mean lower real borrowing costs, making loans more appealing for purchasing homes, business investments, or education funding. On the flip side, high real interest rates increase borrowing costs, dampening borrowing for consumption or investment. High real interest rates might also encourage saving over spending due to the higher real return on savings, while businesses could postpone or scale down new projects due to increased real financing costs.

An increase in real interest rates raises the real cost of servicing debt for individuals, businesses, and governments, leading to higher real debt payments. This reduces available funds for other spending, potentially slowing economic activity as money is shifted from productive investments or consumption to debt servicing. Unlike nominal rates, real rates capture this change in debt's real burden.

Real interest rates also affect the real exchange rate and international trade. Higher real rates can attract foreign investment, leading to a stronger real exchange rate, making exports pricier and imports cheaper. This situation could negatively impact the trade balance and export-dependent industries, further influencing economic growth. Nominal rates, without considering inflation differences between countries, do not have the same impact on the real exchange rate and trade balance.

The motivation behind the Federal Reserve's consideration to lower interest rates soon is the rising real interest rate. Real interest rates provide a more precise understanding of the economic implications of interest rate adjustments since they take inflation into account. This allows for a clearer view of the real cost of borrowing, the actual return on investments, and the genuine economic incentives for savers, investors, and consumers. Without this context, nominal rates might conceal the true economic conditions, particularly in times of fluctuating inflation.